Disability* Insurance

(* plus Medical, Dental, Vision and Life insurance too)

Beauty and Cosmetology Industry

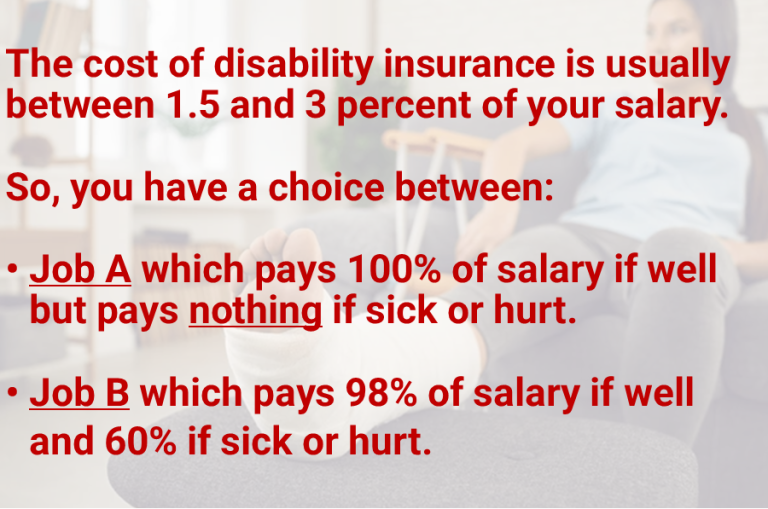

Disability insurance keeps a paycheck coming to you if you cannot work due to illness or injury.

Serving the beauty and cosmetology industry...

• Hair Stylists

• Nail Technicians

• Massage Therapists

• Pet Groomers

• Estheticians

• Makeup Artists

• Lash and Brow Specialist

• Anyone who is self-employed

• Any employer who wants to offer benefits to their employees.

Some common reasons stylists file disability claims:

- Repetitive Strain Injuries (RSI):

- Carpal Tunnel Syndrome: Caused by repetitive motions like cutting, styling, or using scissors/clippers extensively.

- Tendinitis: Inflammation or irritation of a tendon, often from repetitive hand and wrist movements.

- Back and Neck Pain:

- Constant standing, bending over clients, and maintaining awkward postures for long periods can lead to chronic back or neck strain or conditions like herniated discs.

- Skin Conditions:

- Contact Dermatitis: Exposure to hair dyes, shampoos, conditioners, and other chemicals can cause allergic reactions or irritation on the skin of the hands, arms, or face.

- Musculoskeletal Disorders:

- Conditions like arthritis can make the physical demands of hairstyling, such as holding tools or standing for extended periods, extremely painful or impossible.

- Vision Problems:

- Eye strain from precision work or chemical exposure from hair treatments can exacerbate or lead to vision issues.

- Mental Health Issues:

- The stress of dealing with clients, managing a business, or the physical toll of the job might lead to conditions like anxiety or depression, which can be debilitating enough to warrant a disability claim.

- Autoimmune Diseases:

- Conditions like rheumatoid arthritis, lupus, or fibromyalgia can severely impact a hairstylist's ability to work due to joint pain, fatigue, or other systemic symptoms.

- Injuries from Accidents:

- While not work-related, accidents outside of work (like falls, car accidents) can result in injuries that prevent hairstylists from performing their job.

- Respiratory Issues:

- Long-term exposure to hair chemicals or salon environment pollutants might lead to respiratory conditions like asthma.

- Pregnancy Complications:

- Some hairstylists might need to file for short-term disability due to complications related to pregnancy or if advised by healthcare providers to avoid exposure to certain chemicals.

Replace lost personal income in the event of disability.

Start coverage now to lock in rates and increase coverage as your income and needs increase.

Fully portable to take with you to any employment. Up to $30k in monthly benefit.

Medical, Dental, Vision & Life Insurance

Yes - we are here for these coverages too!

We've all heard of Medical, Dental, Vision and Life coverage so not as much explanation is necessary for these coverages as Disabilty. But they are important and if you are in need of coverage, click the button on the form below and we'll be glad to get quotes for you!

Let's get a no-obligation quote started!

Getting a quote is a great way to just get some information. You are under NO OBLIGATION to enroll in coverage.

Name, sex, email and Date of Birth are required, but please complete the other info below to the best of your ability.

Fully customizable.

You choose the options that best fit your personal needs.

It can be confusing! We're here to help and answer questions every step of the way.

Some important definitions below associated with how you choose to customize your coverage.

Definitions of Occupation

How the occupation of the client is defined is one of the most important policy differentiations. In general, if we can get it, we want to the client to be able to receive benefits if he or she is unable to perform his or her occupation, but that does not mean that the strongest (and most expensive) necessarily makes sense for everyone.

In the private insurance market there are basically four definitions of disability, described here from strongest to weakest:

- Own Occupation or Regular Occupation (sometimes True Own Occupation): The inability to perform the substantial and material duties of your occupation—this definition would allow the client to work in another occupation and still collect all of his or her benefit, regardless of how much he or she might earn in the new occupation, if disabled from their original occupation. This feature is very popular with physicians, dentists and attorneys. In theory, a surgeon could continue to collect his $20,000 of monthly benefit, for example) and could make a million dollars a year as an insurance agent.

- Transitional Own Occupation: This definition is similar to the own occupation and differs only if the client chooses to work in a different occupation. In that circumstance, the carrier will compare the new income of the client in combination with their benefit amount with their pre-disability earnings. If the new income and benefit amount are less than the pre-disability earnings, the client will continue to receive the full benefit (same as the true own occupation definition). However, if the new income and the benefit combined exceed the pre-disability earnings, then the carrier will reduce dollar for dollar the benefit amount (one carrier has a floor of 25% of the benefit in this type of scenario). Since this makes the client whole even if working in another occupation, it is popular with physicians and dentists.

- Own Occupation and Not Working (or not engaged): The inability to perform the substantial and material duties of your occupation and not working. The "and not working" is what differentiates this from the true own occupation definition. For most occupations, this definition is what we recommend, if we can get it. The vast majority of all clients who return to work after being disabled return to their same pre-disability profession—this is particularly true for executives and small business owners. It is rare even for physicians to work in different occupations after being disabled from their own. The key here is that clients are protected in their occupation as long as they do not choose to work in a different occupation—and the carrier cannot force them into a different occupation.

- Any Occupation: Often this definition comes with language that relates the definition of disability to the client’s level of training and experience, but do not be fooled. With some occupations or health conditions, however, it is the best that can be offered.

Elimination Period

The elimination period functions as a deductible—it is the period of time that must elapse from the start of the disability until benefits are paid. For individual disability policies, the most common elimination period is 90 days. But this means that the client must self-insure for that time period. Shorter and longer elimination periods are available, but shorter periods are significantly more expensive and longer periods offer only limited savings.

Benefit Period

The benefit period is the amount of time that a policy will pay benefits. In general, for individual policies, we recommend a “to age 65” or “to age 67” benefit period to protect clients in the event of a truly catastrophic event, but we are also firm believers in the idea that some protection is better than no protection. The average claim is about 5 years in length, so if a client cannot afford a benefit period to age 65, you will still do them a service by helping them buy a five or even two year benefit period.

We need your consent to load the translations

We use a third-party service to translate the website content that may collect data about your activity. Please review the details in the privacy policy and accept the service to view the translations.